Political theatre returns

Politics is a continuum – it will ebb and flow sometimes quickly and violently. I had hoped after the July 2024 general election it would stay quiet for a while. I felt the country needed and deserved a period of calm, after the chaos that had characterised the period since June 2016.

However almost immediately, the honeymoon period was over, the UK press and online media engaged in endless carping and excessive criticism of the new government. This has not been effectively countered by No. 10 communications. The fury directed against the PM felt weird given his recent appointment and lack of anything earthshattering. The US Presidential election of 2024 threw new curveballs in all directions, destroying previous norms, creating issues that demanded the new PM’s attention.

The PM has done well managing a nearly impossible international context, notably by not getting involved in the US/ Israel/ Iran conflict, for the right reasons. The PM also stood up for Greenland at a critical time in January 2026, ‘the future of Greenland is for its people and the Danish government alone’. The PM’s stance on Greenland was pivotal in preventing a blatant US land grab that would have destroyed NATO. On foreign policy the PM has navigated the UK through troubled waters, frequently facing public insults from the US leadership, and got virtually no credit for it.

Alas, change is now afoot, despite the Government’s massive Commons majority, which appears irrelevant if political fracturing occurs and parties degenerate into factions and infighting.

Domestically, what was Starmer’s crime? I suppose promising change and not delivering at a speed the country desired or had assumed was possible. The 2024 election was a vote for change, but change takes time, and rapid change is exceptionally difficult in the context of stagnant GDP and a permanently volatile international situation where a vulnerable UK is constantly bracing itself from shock events, wars / trade wars etc.

One charge levelled at Labour is it is not doing enough to tackle Britain’s generational disparities that have, and continue to create, real dysfunction and injustice in young people’s lives. The Gen Z category is facing massive debt burdens early on, and significant difficulty buying a home, unlike previous generations, at least in modern times. The inability of many Gen Z to break parental dependencies, having to delay adulthood, is an issue festering for over a decade. Gen Z is now facing the added hardship of a challenging youth job market, high unemployment and artificial intelligence which is hurting entry-level jobs.

Meanwhile, Gen X (1965-1980) is pulling away in asset terms, receiving Baby Boomer inheritances, and facing far lower income risks. Gen X are arguably AI beneficiaries as they control AI deployment.

Cost pressures have also weighed heavily, exacerbated by the international context which, as C-19 proved, remains sensitive to any supply shock.

This problem is not like the ideological battles of the 1970s / 1980s that were resolved by one party bulldozing through. How precisely does any PM tackle generational poverty in 2 years? It is ludicrous to suggest anyone can achieve this. Should the UK government provide free housing for a generation? Can it pay off / underwrite or assume all student debt?

There is a major problem with ditching the PM now. Any new PM will face the same problems, that have no quick solution, and significant pressure for a General Election to obtain a new mandate away from Labour’s 2024 manifesto. That would be the signal for more significant structural change. It is similar to Theresa May’s problem in 2016. She had wanted her own mandate. Her political inheritance was deemed insufficient, she then called the snap election in June 2017, and everything went into reverse from there.

A general election in 2026 would likely be destabilising, it would generate significant new uncertainty. Both in the run-up and post, it would risk a re-run of the Truss episode.

But Thursday 7th May 2026 saw a remarkable glimpse of a possible future UK political landscape, one where UK has five political parties, each capable of winning meaningful seats in Westminster, armed with similar levels of public support. Moving to a 5 party configuration at the next election, from 3 presently, would result in fragile combinations and coalition deals, and more political polarisation / dissent.

Should these voting patterns be transmitted to the central government, as these local government results have proved, there would be increased political volatility that would make it even harder for UK leaders to achieve the ‘change’ the country desires.

Pre-2016 the UK was considered a ‘safe haven’ at least in terms of political stability. Brexit destroyed that. Sterling has never recovered its pre-Brexit levels against either the USD or Euro. But if this shift is real, it could mean an even weaker sterling and increased risk premia for holding UK assets.

A ‘measured’ response so far

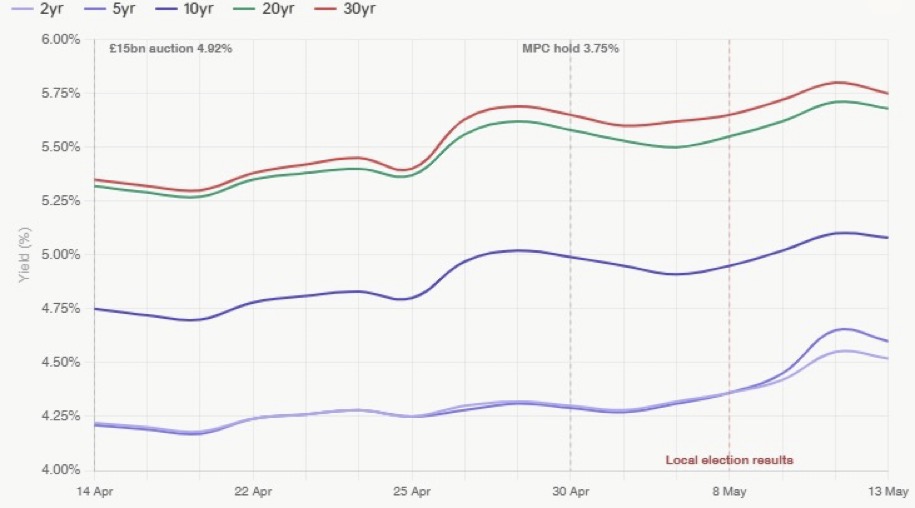

There has been a marked shift up in the UK yield curve with most of the move since 8th May 2026.

Source: CSS Investments Ltd

- Gilt yields: impact is pronounced at the long end (30 YR 5.80% +33bps (over month) +80bps (over 3 months). The 20 YR moved up to 5.62% + 24 bps (over month). The 10-year yield is offering 5% for the first time since 1998. The short end move is more modest, with the pressure points in mediums and long dated.

- Rate futures: the 2-year gilt is paying 4.55% a massive 0.8% above Bank Rate at 3.75%; hence market expectations have shifted to very hawkish, pricing in three rate hikes to 4.50% by end 2026. The MPC might take a more measured view at its 12th June meeting, but might not. Investors are pricing in sharply higher 2026 inflation due to the ongoing Gulf conflict / crude oil impact. However, it was only February when expectations were for a small rate cut over 2026. Again, a textbook response, wars are inflationary as we are taught early on in economics studies.

- UK blue chips have held up with negligible net change over the week – a telling pointer that global events, commodity prices, the earnings season, takeover activity is more relevant or at least offers sufficient distraction.

- UK mid-caps are usually the most sensitive to UK factors, the leading index has lost 0.75% since 8th May, a muted response.

- Sterling is vulnerable in this scenario. It is early days but so far it is holding up range bound. There is no sterling crisis yet.

Source: CSS Investments Ltd

Conclusion

Patience is a virtue in capital markets, as opposed to being prevalent in the voting public where impatience is on display now. The PM has been judged and treated harshly – there is no simple magic wand to the UK’s issues.

The investor response has been mild so far with only a few areas, long gilts, rate expectations seeing tangible change i.e. a repricing.

It remains possible the heat will be taken out of this, again, if cooler, wiser heads prevail. Politics is about numbers and momentum. A credible challenge, even if mounted, could yet fail for lacking either or both.

The current investor mindset may yet prove rather complacent. That said, as summer kicks off, opportunities may well emerge in the sectors recently hit hardest, housebuilders, airlines, leisure retailers, broadly speaking most of the C-19 ‘usual suspects’. We are sure 2026 will serve up a few more curveballs and soon.